Sold JPM, No More Banks Among My Chosen Assets

Latest developments from inflationary data and US central bank authorities have encouraged me to take profit on my only stock from the banking segment, a moderate stake in JPMorgan Chase & Co (JPM). You may wonder what happened to this reputable financial institution or its ratings, or just to my personal assessment of its reliability. Everything is OK with JPMorgan ever since it was established more than 150 years ago. In fact, I still consider JPMorgan as the strongest representative of the US banking family, and that was exactly the reason why I left a block of my JPM stock in peace after selling out all other banking stocks. So, the point is I feel the banking segment may form the weakest link among broader sectoral distribution of Wall Street investments, as I don't believe anymore that the squeezed financial income by US banks may be hold unharmed when the benchmark 10-year public bond yields exceeded 4.5%, for the first time since late November.

Specifically, too high bond yields may further drop the value of most previously accumulated old bonds on the balance sheet of large and small banks, indiscriminately. Historically high borrowing costs is the reason behind the curtain of this piece, where the Federal Reserve wrote the screenplay of this sad episode. Again, expensive costs for credit financing, from the banking customers point of view, makes their need for credit lower, weakening the source of regular income for banks. Borrowing costs, as well as bond yields, cannot follow below certain high standards when the interest rate cuts phase of a monetary cycle is postponed due to persistent inflationary pressure.

The Federal Reserve (Fed) Minutes this Wednesday have clearly confirmed to me that most of the Fed members are ready for a longer period of tight policy. "Some" of them literally agreed that the current 5.25%-5.50% interest rate range was "less restrictive than desired, which could add momentum to aggregate demand and put upward pressure on inflation". This is exactly a train of thought, which is used from time to time in the periods of arguing the need for even more rate hikes, and not rate cuts. Well, no policy makers actually pencilled a higher policy rate on dot plot projections, yet it is now hard to imagine any rate cut at least before September. The Fed has no reason to cut, as they need to wait two or three consecutive quarters with declining CPI (consumer price index) numbers, while the CPI is surging at the moment. Central bankers seem to be not sure about inflation dynamics in coming summer months with usually growing gasoline prices, as Minutes also showed they were debating whether it became risky to ease too soon, before the inflation path shifted back towards the major supposed autobahn leading to its 2% target. "Participants generally noted their uncertainty about the persistence of high inflation and expressed the view that recent data had not increased their confidence that inflation was moving sustainably down to 2%," the minutes said in favour of two opposite views in one sentence. Such rhetoric looks like replacing some portion of lies. This was a bad sign.

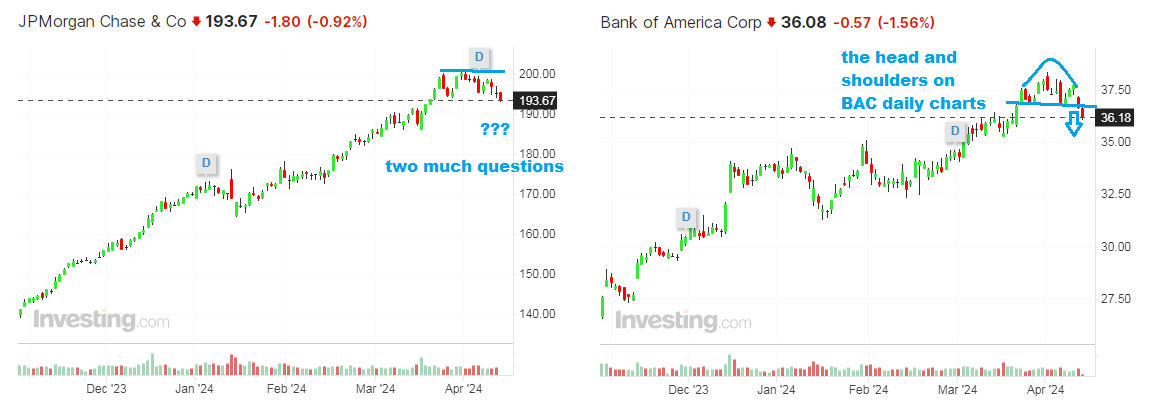

Share price of the Bank of America (BAC) quickly lost nearly 3% for the last two trading sessions. Technically, the Bank of America formed a potential top to slide down further, after the head and shoulders pattern appeared on daily charts and the neckline was broken just a day ago. Meanwhile, as the segment's undisputed leader, JPM has wasted only about 1% so far. Yet, the uptrend in JPM is under question as well. So, this does not look reasonable to squander the big advantage after the JPM price climbed up from a $150 area to about $200 per share from the pre-Christmas time to this spring. No prudent owner will leave it to chance, especially when the cut of cards will look more and more unfavourable. This is why I don't want to wait for the earnings date, which is scheduled for tomorrow, Friday April 12, when JPM and some other large banking players like Blackrock, Wells Fargo and Citigroup would reveal their quarterly numbers, as Q1 numbers do not matter too much when the hurricane on bond yields is already here.

The banking rally accelerated in the first three months of the year, hand by hand with a bias towards cutting rates. Previously, they projected cutting rates by 0.75%, and now the crowd began to understand that even a 0.5% rate cut would be a sweet dream scenario for 2024, when the single rate cut just two months before the November elections to the White House would be like throwing us a bone, just for the bulls would not suddenly transform into bears in the improper time.

Disclaimer:

The comments, insights, and reviews posted in this section are solely the opinions and perspectives of authors and do not represent the views or endorsements of RHC Investments or its administrators, except if explicitly indicated. RHC Investments provides a platform for users to share their thoughts on financial market news, investing strategies, and related topics. However, we do not guarantee the accuracy, completeness, or reliability of any user-generated content.

Investment Risks and Advice:

Please be aware that all investment decisions involve risks, and the information shared on metadoro.com should not be considered as financial advice. Always conduct thorough research, seek professional advice, and exercise caution when making investment decisions.

Moderation and Monitoring:

While we strive to maintain a respectful and informative environment, we cannot endorse or verify the accuracy of all user-generated content. We reserve the right to moderate, edit, or remove any comments or posts that violate our community guidelines, infringe on intellectual property rights, or contain harmful content.

Content Ownership:

By submitting content to metadoro.com, users grant RHC Investments a non-exclusive, royalty-free license to use, display, and distribute the content. Users are responsible for ensuring they have the necessary rights to share the content they post.

Community Guidelines:

To maintain a positive and respectful community, users are expected to adhere to the community guidelines of Metadoro. Any content that is misleading, offensive, or violates applicable laws and regulations will be subject to moderation or removal.

Changes to Disclaimer:

We reserve the right to update, modify, or amend this disclaimer at any time. Users are encouraged to review this disclaimer periodically to stay informed about any changes.