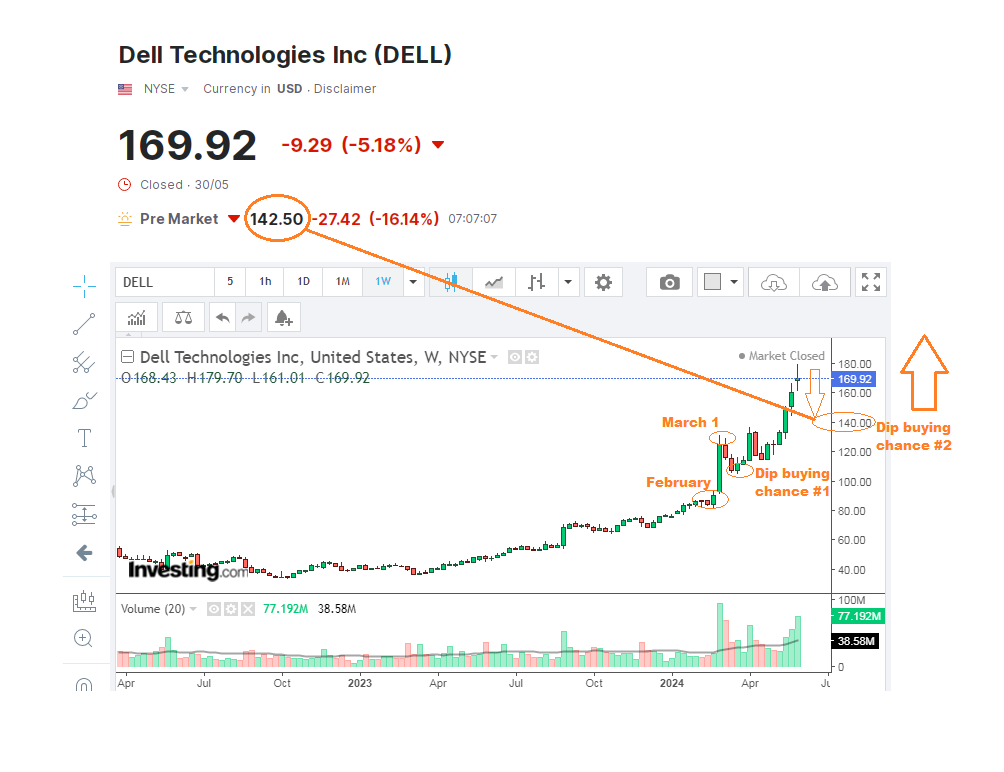

Another Moment for Dips Buying in Dell

Good Wall Street morning to everybody. Why do I consider this last morning of May as actually a good one? Because it gave me a good opportunity to buy even more shares of Dell at an amazingly low price. Indeed, a rapid 20% correction, from an all-time high at $179.70 just two days ago (on May 29) to $142.50 per share right at the moment, cannot be normally justified by the company’s own forward guidance, which was slightly lower than consensus estimates, while its Q1 results were brilliant. The reasonable background behind this mad overnight shift to a discounted trading in after-hours is rather of a technical nature, as Dell stock became overbought following its equally mad recent rally from $85 in February to almost $180 in May. This was too fast for an old and stable IT business.

I sought a chance to buy Dell within a $105-110 price range after the stock already soared to $130 on March 1. I found this opportunity when the market gave it to all of us, after a couple of weeks of waiting in an ambush, and so I used that chance. Yet, the current price of just above $140 after the peak of nearly $180 is an equivalent of nearly $100 after a previous peak of $130, and so the whole situation repeats itself at new levels.

So, this market is so merciful to indecisive traders to allow us another fantastic purchase opportunity in less than three months.

What were the fundamentals urging Dell shares to fall? The computer world giant reported its quarterly sales of $22.2 billion vs average analyst pool bets on $21.65 billion. This was also a 6% surplus compared to the same quarter of 2023. Dell’s Infrastructure Solutions Group is a standout performer, with the division’s revenue adding 22% YoY to $9.2 billion, helped mostly by a record 42% increase in servers and networking sales. This is great, or I am a space cadet fool. It was only the Client Solutions Group which remained flat YoY, while commercial client sales were at a 3% annual rise (not so high). The company's chief financial officer, Yvonne McGill, pronounced the magic two-sound mantra (not AUM, but AI) on artificial intelligence influence on the company's achievements. What else does the market need to return to the growing rally soon?

Dell's adjusted income (earnings per share, or EPS) was $1.27, also slightly above the analyst estimate of $1.25. The only disadvantage was that this profit number showed a 3% decrease vs the first quarter of the previous year. And does it cost a 20% discount for the shares price? You would better judge it yourself.

It certainly feels like this exclusive market volatility in Dell Technologies stock or, most of all, my regular posts on this issue (ha-ha) would make Dell shares a top choice financial instrument for private investors. Well, it is already very popular, because it’s moving like another meme stock, though its market caps (and thus, the ability of its next price moves to be forecasted) is 15 to 100 times more than the market caps of some hyping Reddit’s collective brainchild like GameStop and AMC. Let me hope this explosive combination of reasons would only attract many “newcomers” (in terms of never thinking on trading Dell before). Again, portfolio investors used to trade more solid flagships like Google or Amazon, but many of them became tired from disappointing behaviour of Tesla or Apple since the beginning of 2024. For all these groups of Wall Street inhabitants, a possible Plan B may include using some part of their trading volumes to trade a middle layer of IT stocks, which is also going to grow further on the AI, big data and cloud agenda. For me, DELL could be in a short-list of such assets.

Disclaimer:

The comments, insights, and reviews posted in this section are solely the opinions and perspectives of authors and do not represent the views or endorsements of RHC Investments or its administrators, except if explicitly indicated. RHC Investments provides a platform for users to share their thoughts on financial market news, investing strategies, and related topics. However, we do not guarantee the accuracy, completeness, or reliability of any user-generated content.

Investment Risks and Advice:

Please be aware that all investment decisions involve risks, and the information shared on metadoro.com should not be considered as financial advice. Always conduct thorough research, seek professional advice, and exercise caution when making investment decisions.

Moderation and Monitoring:

While we strive to maintain a respectful and informative environment, we cannot endorse or verify the accuracy of all user-generated content. We reserve the right to moderate, edit, or remove any comments or posts that violate our community guidelines, infringe on intellectual property rights, or contain harmful content.

Content Ownership:

By submitting content to metadoro.com, users grant RHC Investments a non-exclusive, royalty-free license to use, display, and distribute the content. Users are responsible for ensuring they have the necessary rights to share the content they post.

Community Guidelines:

To maintain a positive and respectful community, users are expected to adhere to the community guidelines of Metadoro. Any content that is misleading, offensive, or violates applicable laws and regulations will be subject to moderation or removal.

Changes to Disclaimer:

We reserve the right to update, modify, or amend this disclaimer at any time. Users are encouraged to review this disclaimer periodically to stay informed about any changes.