Oracle Is Not Going To Lose This Game

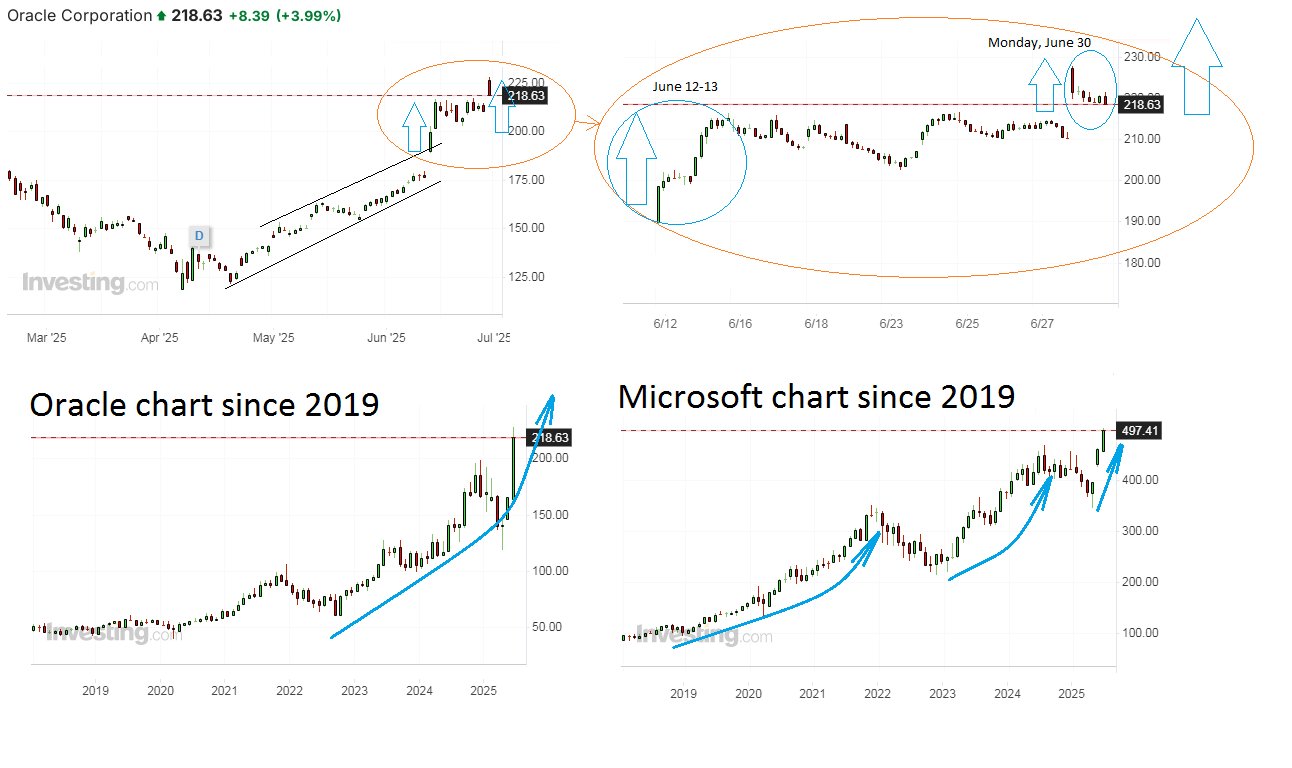

Oracle's recent high of $228.22 during the last trading session of June, quickly followed by a nearly $10 pullback to $218.63 closing, offers a good chance to add the company to one's stock portfolio if it hasn't been included yet for some reason. The stock initially soared by as much as 7% soon after the opening bell on June 30 after Oracle's CEO Safra Catz said the company is experiencing a very solid start with continued "robust growth to the fiscal year of 2026. According to Oracle's SEC (U.S. Securities and Exchange Commission) filing, the company’s MultiCloud database sales is growing at over 100% YoY. Safra Catz also cited multiple large cloud services agreements, including one especially big deal to contribute more than $30 billion in annual revenue since 2028.

If so, then this cloud-computing business has created a more than favourable fundamentals behind a new take-off after the weekend, so that retesting already achieved higher levels looks inevitable, which means almost 4.5% of free running to the upside in the coming days. To build the profit handicap is always useful when seeking a proper entry point to popular assets like Oracle. I personally will try to capitalize the situation. This is still attractive, even though Oracle jumped more than 22% on June 12-13 on the heels of its regular quarterly report, from $175 to $215+, but even $250 does not look like the end point of its current round of a climb. This is just another straightening arrow to the top, looks very similar to Microsoft several years ago.

Where did I get the $250 figure now, other than it being round and very nice? This was Stifel analyst group, which freshly upgraded Oracle stock from previously Hold to currently Buy just over the weekend and raised its price target to $250 from $180. Stifel analyst Brad Reback noted a "dramatic increase" in Oracle's capex (capital expenditure) and RPO (remaining performance obligation) to help growth prospects both in the cloud infrastructure and SaaS (software as a service) applications. Oracle's revenue is growing at 8.4% over the last annual period, by the way. Stifel remarked that Oracle’s management has shown skill as its headcount grew only 2% while total operating expenses expanded by 5% and total revenue increased more than 8% in 2025. Stifel guys are projecting a 16% growth in fiscal year 2026 and 20% in fiscal year 2027... much better than now! For some reason I believe them, and my own expectations too. Maybe because Oracle is the heart of a $0.5 trillion Stargate project for building US data centres, together with OpenAI and SoftBank and under the patronage of the Trump-led Republicans for 3.5 years more at least. Baby, don't you know you can't lose under such conditions?

Did you know that according to Forbes data for the middle of June, Oracle co-founder Larry Ellison, of which he owns roughly 40%, was the second-richest person in the world, after his business soared to new peaks. And yes, this man stands just behind Elon Musk, outpacing the wealth of the Venice groom, Amazon's Jeff Bezos and Meta's godfather Mark Zuckerberg. How do you like these apples? IMHO, if you're a small investor but trying to build a solid portfolio that includes Tesla, Amazon, and Meta, of course, then how can Oracle not be there? Again, Ellison sat on Tesla's board in 2019-2022, with his 45 million split-adjusted shares before stepping down as a director. Then probably your portfolio balance and success are relative terms. And in 2020, Ellison reportedly moved to his Hawaiian island Lanai, which he bought nearly all for $300 million. Woody, I'm slipping!.. if you know this line from Toy Story. Living like this, I mean. "When people start telling you that you're crazy, you just might be on to the most important innovation in your life," Larry Ellison once said. Damn, maybe a dozen Oracle shares will make me a little richer than I am now. I've nothing more to tell you. So far, they cost less than $220, not $250 and not $300.

Disclaimer:

The comments, insights, and reviews posted in this section are solely the opinions and perspectives of authors and do not represent the views or endorsements of RHC Investments or its administrators, except if explicitly indicated. RHC Investments provides a platform for users to share their thoughts on financial market news, investing strategies, and related topics. However, we do not guarantee the accuracy, completeness, or reliability of any user-generated content.

Investment Risks and Advice:

Please be aware that all investment decisions involve risks, and the information shared on metadoro.com should not be considered as financial advice. Always conduct thorough research, seek professional advice, and exercise caution when making investment decisions.

Moderation and Monitoring:

While we strive to maintain a respectful and informative environment, we cannot endorse or verify the accuracy of all user-generated content. We reserve the right to moderate, edit, or remove any comments or posts that violate our community guidelines, infringe on intellectual property rights, or contain harmful content.

Content Ownership:

By submitting content to metadoro.com, users grant RHC Investments a non-exclusive, royalty-free license to use, display, and distribute the content. Users are responsible for ensuring they have the necessary rights to share the content they post.

Community Guidelines:

To maintain a positive and respectful community, users are expected to adhere to the community guidelines of Metadoro. Any content that is misleading, offensive, or violates applicable laws and regulations will be subject to moderation or removal.

Changes to Disclaimer:

We reserve the right to update, modify, or amend this disclaimer at any time. Users are encouraged to review this disclaimer periodically to stay informed about any changes.